My Salary Doubled. My Stress Doubled With It. Nobody Warned Me About This.

Let me ask you something honest.

Do you remember the last time you got a raise — a real one — and felt genuinely, lastingly relieved? Not just for a week. Not just until the next credit card statement arrived. Actually relieved, like the pressure had lifted and things were going to be different now?

Most of us can't say yes to that. And if you're reading this, I'm guessing you've lived some version of this: more money comes in, life adjusts to absorb it, and within three or four months you're back to the same low-grade financial anxiety you thought you'd left behind. The number on your payslip goes up. The feeling in your chest stays exactly the same.

I lived inside that loop for eight years. Eight years of promotions, salary hikes, job switches for better packages — and at the end of it, at 33 years old, earning more than I had ever earned in my life, I had almost nothing to show for it. Not in any real, lasting, belongs-to-me way.

For a long time I thought I was doing something wrong. Spending too much on the wrong things. Not disciplined enough. Not smart enough with numbers. I blamed myself in quiet, private ways that I never talked about out loud.

But here's what I eventually figured out — and this is the thing I wish someone had told me at 22, or 25, or even 30:

The problem wasn't my spending habits. The problem was that nobody had ever taught me how money actually works. Not school. Not my parents. Not any manager or mentor I ever had. I had been handed a salary and expected to figure out the rest on my own, using a set of money beliefs I had absorbed from people who were just as lost as I was.

What changed for me wasn't a windfall. It wasn't luck. It was one slow, uncomfortable, occasionally humbling process of unlearning what I thought I knew — and replacing it with something that actually made sense.

I'm going to tell you exactly what that looked like. The mess, the denial, the small wins, the moments I wanted to give up. All of it.

If you've ever felt like your salary is a treadmill that just keeps speeding up, stay with me. Because the way out isn't what you think it is.

The month I crossed ₹1 lakh take-home, I bought myself a watch.

Not an extravagant one. But a real one — not the Fastrack I'd been wearing since college. A proper watch, the kind with a clasp that made a satisfying sound. I told myself I deserved it. I had worked for three years at a company that constantly promised and under-delivered, and I had finally jumped ship for a role that recognized my worth.

I remember standing at the counter and feeling something close to arrival. Like I had crossed into a different category of person.

Six months later, the watch was on my wrist and I was borrowing ₹15,000 from my younger brother to cover rent while I waited for a delayed expense reimbursement. I didn't tell him what it was for. I said it was for something medical.

That lie — small, practical, born of pure embarrassment — was the moment I knew something was genuinely wrong. Not with my income. With something deeper that I didn't have language for yet.

If you'd looked at my life from the outside that year, you'd have seen someone doing fine.

Good job title. Decent apartment in HSR Layout — not the fanciest part, but respectable. A bike I'd upgraded from my old one. Evenings out with friends who were all in roughly the same situation, which meant we collectively normalized spending in ways none of us could truly afford. Brunches on Sunday. Trips planned on EMI. Gadget upgrades timed to festival sales that turned into twelve-month no-cost loans that were, it turned out, not as no-cost as advertised once you read the fine print.

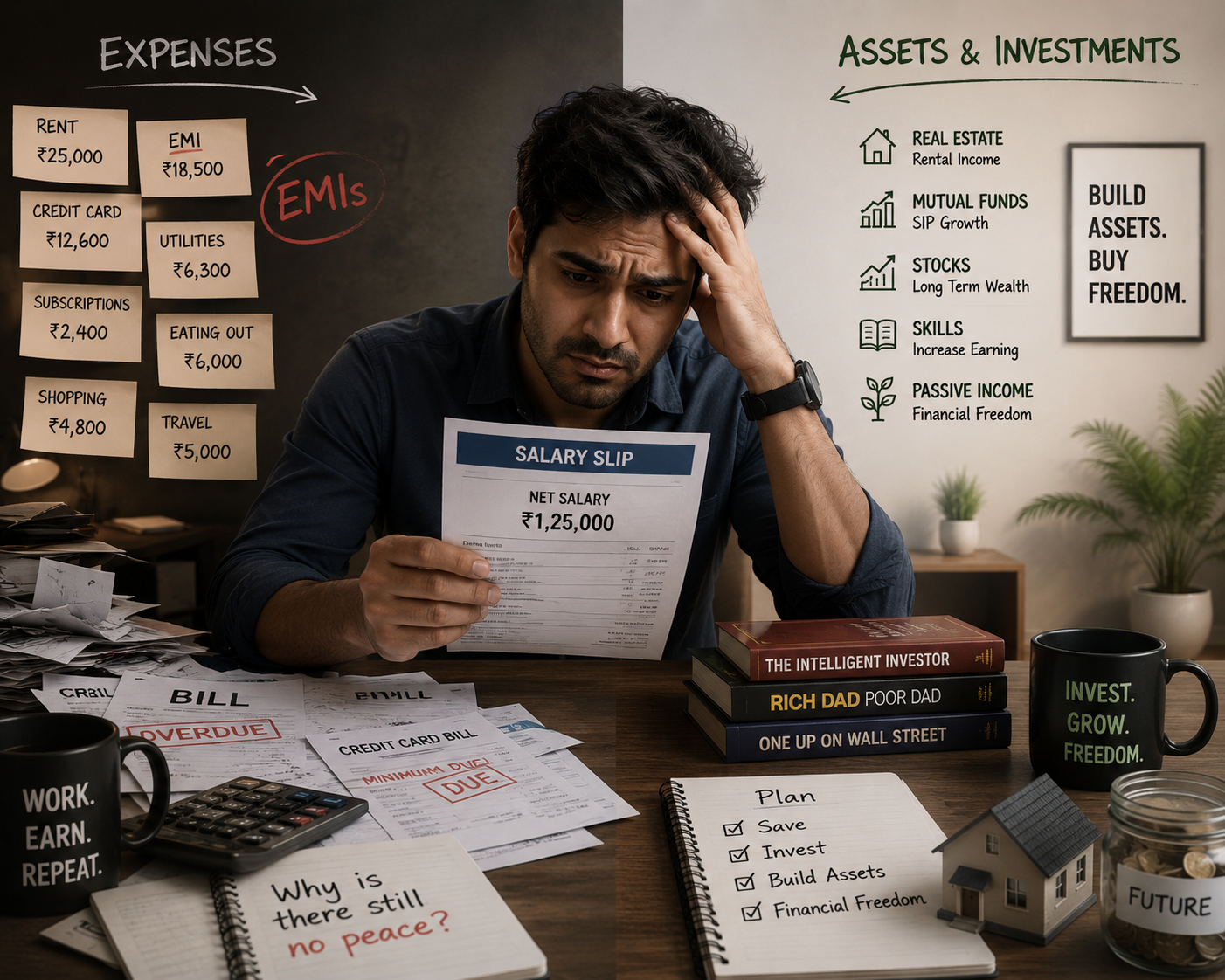

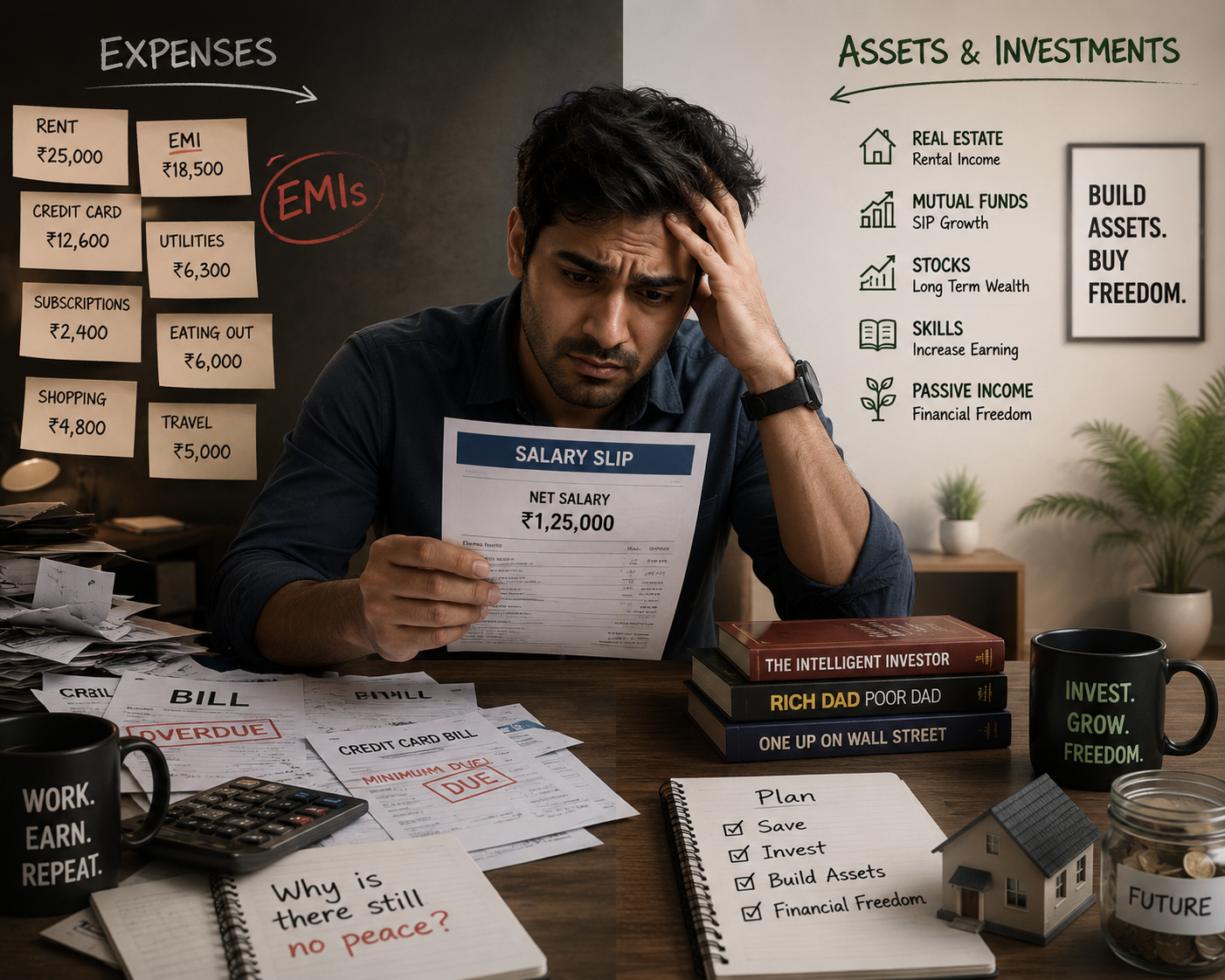

My salary had grown steadily. At 25, I made ₹42,000 a month. At 28, ₹67,000. At 33, just over a lakh. Each jump had felt significant. Each jump had been followed, within a few months, by expenses that perfectly matched it.

New salary, new rent because the old apartment felt a little small now. New salary, new phone because the old one was slowing down. New salary, new subscriptions, new weekend habits, new version of normal that cost exactly as much as the new normal paid.

I kept waiting for some salary level where there would finally be breathing room. Where the math would stop being so tight. I kept assuming that number was just slightly ahead of wherever I currently was.

It never arrived.

The person who broke this open for me was not who I expected.

Her name was Kavitha. She ran a small gifting business from her apartment — custom corporate hampers, festive packaging, that sort of thing. I'd met her through a common friend and we'd stayed loosely in touch. She was a few years older than me, had never held a corporate job for more than two years, and drove a car that was visibly older than mine.

By every visible metric, I was doing better than her.

Then one evening she mentioned, in the most casual way possible, that she'd just "picked up another property" — a small commercial space she was renting out to a tutoring center. She said it the way you'd mention picking up groceries.

I did the math in my head. The rent from that space alone was probably covering her car EMI, her utility bills, and her phone. From one thing she owned. While she slept.

I asked her, more directly than was probably polite, how she had managed to do that.

She shrugged. "I stopped spending money on things that cost me more money. And I started spending it on things that made me money.

I asked her what that meant practically. She looked at me for a moment like she was trying to gauge how serious the question was.

"Your car," she said. "Does it pay you anything?"

"No."

"Does it cost you every month?"

"EMI, insurance, fuel... yeah."

"That's a liability. It takes money from you. Now" — she tilted her head — "what do you own that pays you?"

I thought about my fixed deposit. ₹40,000, sitting in a bank, earning maybe 5.5% annually.

"FD," I said. "And my PF."

"Okay. So your money is mostly parked, and most of what you own costs you monthly. And you earn more, so you spend more, and the gap never really closes."

She said it gently. But it landed like something heavy.

"Nobody teaches this," she said. "They teach you to get a salary. They don't teach you what to do with it."

I went home that night and did something I had been avoiding for approximately three years.

I wrote down every single thing I spent money on each month. Not a rough estimate. Every EMI, every subscription, every "small" expense I usually didn't count because it felt too minor to matter.

The total was ₹83,400.

I made ₹1,02,000.

After taxes, I took home roughly ₹84,500.

I was, functionally, spending everything I made. Sometimes more. The credit card rollovers and the occasional loan from family were not emergencies. They were the structural result of a system with no room in it, running at 98% capacity every single month.

I stared at that page for a long time.

Then I did a second exercise that Kavitha had suggested. I drew a line down the middle of a fresh page. Left side: Assets — things I owned that paid me. Right side: Liabilities — things I owned that cost me.

Left side was nearly empty. A small FD. PF contributions I couldn't access for decades. That was it.

Right side filled up fast. Bike EMI. Old personal loan I was still paying off from a trip I barely remembered. Two credit cards carrying balances. A laptop EMI. The watch, technically, if I counted the credit card I'd put it on.

It was not a balance sheet. It was a confession.

I want to be honest about what happened next, because it wasn't clean.

I didn't immediately transform. I didn't wake up the next morning with a plan and execute it flawlessly. I read things, half-understood them, got overwhelmed, and closed the browser tab. I started a budget spreadsheet three times and abandoned it twice. I had whole weeks where I told myself I'd deal with it "after this month" and then didn't.

What finally broke the inertia was a small, almost embarrassingly simple change.

I set up an automatic transfer of ₹8,000 to a separate account the day my salary came in. Before rent. Before bills. Before anything. Just ₹8,000, gone from my main account before I could psychologically claim it as available.

The first month, I panicked halfway through and almost transferred it back.

I didn't.

The second month was uncomfortable but manageable.

The third month, I barely noticed. My brain had adjusted to treating ₹8,000 as not-mine, and had quietly found ways to cope with the slightly smaller number without me having to consciously fight for every decision.

After four months, I invested it. Index funds — the most boring, unsexy, low-maintenance option I could find after reading more than I ever expected to read about mutual funds. No stock tips. No crypto. No friend's "sure thing." Just a broad market fund, SIP, automatic, don't touch it.

The first returns were ₹300-something.

I know how that sounds. Three hundred rupees. After four months of discipline and discomfort.

But I took a screenshot. Because it was money that had moved toward me without me trading an hour of my life for it. The direction was new. The direction was the whole point.

There was another shift happening around this time that I didn't fully recognize until later.

I had always, at every job, gravitated toward the technical parts of my work. The parts where I could sit quietly and produce something without having to sell it, present it, or convince anyone of its value. I was good at my actual job. I was uncomfortable with everything around it.

My manager had been pushing me toward client-facing work for over a year. I had been resisting it with excuses that sounded professional but were really just fear dressed up in business language.

But I had been reading, in all this financial education I was suddenly consuming, that the skill which showed up again and again in the context of people who built real wealth was the ability to communicate value. Sales, negotiation, persuasion — the ability to make someone else understand why something was worth their money or their time or their trust.

I had always thought of that as a personality type I didn't have. I was slowly starting to understand it as a skill I hadn't developed.

I took the client meeting my manager offered. I was stiff. I over-prepared and somehow still felt underprepared. I talked too fast. I answered questions that hadn't been asked because I was nervous about the ones that might be.

But I took notes. I watched how my colleague Sameer moved the conversation. I paid attention to what made the client lean in and what made them glaze over.

I took the next meeting. And the one after that.

I was not good at it quickly. I was better at it gradually. And "better" turned out to be enough.

Within a year, I had three small consulting clients of my own — small businesses who needed exactly the kind of operational thinking I'd spent years doing for someone else's company. I charged less than I probably should have at first. But I was building something that was, technically, mine. Something that paid me on its own logic, not just in exchange for showing up somewhere five days a week.

The tax conversation happened because of a chance meeting with a CA at a friend's dinner.

I had always thought of taxes as fixed. You earn, a percentage disappears, that's the deal and there's nothing to discuss. The CA — a quiet, precise man named Venkat — raised an eyebrow when I said this.

"You're a salaried employee with no registered structure?" he asked.

"Yes."

"So you're taxed on your full income before you see it."

"Right."

"Do you know that someone with a registered business pays tax on what's left after expenses? Laptop, internet, relevant travel, professional development — many things that you're probably spending money on anyway become deductible?"

I did not know that.

"The law doesn't treat everyone the same," Venkat said. "It treats income categories differently. Most people never learn this because no one who benefits from their not knowing it is motivated to teach them."

He wasn't saying anything illegal. He was saying that the tax system had different rules for different structures, and that educated employees mostly operated in the most taxed category by default, while never being told there were other options.

I registered a proper structure for my consulting work within two months of that dinner. The tax difference in the first year wasn't dramatic. But it was real. And the concept — that systems have rules that reward those who understand them and quietly drain those who don't — had permanently changed how I looked at everything.

I'm writing this almost three years after that evening with Kavitha and her offhand comment about "another property."

I don't own property yet. I want to be straightforward about that. I'm not going to dress this up into a transformation arc that ends with me financially free at 36. That would be dishonest, and I think you'd feel it.

What I can tell you is this:

My asset column has things in it now. Real things, not just parked savings. A growing SIP portfolio. My consulting income, which has become consistent enough that I don't think of it as a side thing anymore. A small fixed-income investment I made last year that pays out quarterly.

My liability column has shrunk. Both credit cards paid in full every month. Personal loan gone. I didn't upgrade my bike when I probably would have before, because I asked myself whether a newer bike was an asset or a liability and the answer was immediate and obvious.

The background noise in my head — the low hum of financial anxiety that I had lived with so long I'd stopped noticing it — has quieted significantly. Not gone. But quieter.

And the thing I keep coming back to, the thing I would tell my 25-year-old self if I could, is this:

The salary was never the problem. The problem was that I had been educated, very thoroughly, in everything except how to handle the salary. I knew how to earn. I had no idea how to build. Those are completely different skills, and only one of them was ever taught to me.

If you're in the loop — earning more, spending more, never quite ahead — it's probably not a discipline problem. It's probably an education problem. The kind of education no one gave you, which means you have to go get it yourself.

That part is annoying. It shouldn't have to work this way.

But it does. And the earlier you start, the more time the math has to work in your direction instead of against you.

*Disclaimer: This scenario was created to explain the key lessons of Rich Dad Poor Dad. Full credit for the original ideas belongs to the author.

1 Comment

Your all blogs are for life changes appreciate your work